The Securities and Exchanges Board of India (SEBI) has further tightened the regulations for the Initial Public Offerings (IPO) by Small and Medium-sized Enterprises (SMEs) in a bid to protect investors in view of the rising concerns as SME IPOs continue to see increased investor participation. Key amendments include profitability requirements, capping of offer-for-sale and doubling of application size among others.

The reforms are aimed at increasing transparency in the SME IPO market and protect investors.

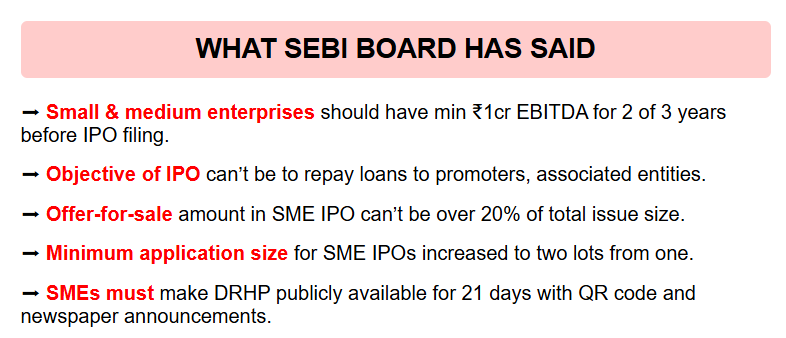

SME IPO norms: key changes

- Profitability Criteria: SEBI’s changed profitability criteria requires the SMEs planning to launch IPO to have a minimum operating profits or EBITDA of Rs 1 crore for at least two out of the three previous financial years.

- Limitation on Selling Shareholders: The market regulator has capped the selling shareholders’ Offer-for-sale (OFS) component at 20% of the total issue size. Also, the selling shareholders now can not offload more than 50% of their existing holdings in the company.

- Phased Lock-in for Promoters’ extra shares: Any shares held by the promoters beyond the Minimum Promoter Contribution (MPC) will now be gradually released. Half of the excess shareholdings would be unlocked after one year and the remaining half after two years.

- Allocation methodology: The allocation methodology for NIIs will now be same as used in mainboard IPOs.

- Application Size doubled: SEBI has changed the minimum application size for SME IPOs to two lots from one lot before, making it harder for small and susceptible investors to get influenced by escalating share prices, social media buzz or grey market premium.

- GCP capped: The SMEs are now only allowed to allocate up to 15% of the total issue size or Rs 10 crore, which is lower, for general corporate purpose (GCP) in the IPO.

- Promoters’ loan repayment barred: The SMEs can now not use the net proceeds from the IPO to repay the loan taken from the promoter, promoter group or any related party, whether directly or indirectly.

- DRHP publishing mandatory: SEBI has notified that the upcoming SMEs have to make their draft red herring prospectus (DRHP) publicly available for 21 days, publish announcements in newspapers and include a QR code. The DRHP should be made available on the website of the SME exchange for public comment and also on the websites of the issuer and merchant bankers.

- Allowance of further issues: SEBI will now allow the SMEs to raise funds through further issues without migrating to the mainboard exchange, if the companies comply with the SEBI (LODR) rules.

- RTP compliance: The SMEs once listed will have to comply with the related party transaction (RTP) norms that are applicable to mainboard listed companies.

What is causing stricter rules?

Recent years have witnessed a flood of SME IPOs as the year 2024 saw debut of around 240 SME IPOs which combined raised over 8,700 crore. And in some instances, the SEBI took notice of the some concerning practices.

- Some SMEs were found to present an ‘unrealistic picture’ of post-issue operations, as per SEBI.

- A report in 2024 also stated that few investment banks were under scrutiny for charging fees as high as 15% of the raised funds, disproportionate to the normally charged 1-3%.

- Few of the SME IPOs also came under scrutiny due to the market manipulation where non-genuine bids were placed to ensure oversubscription, inflating investor interest and demand for the stock.

The full notification can be viewed on the SEBI website here.